Forecasting the economic situation in 2023

The world economy still faces many risks from 2022, such as the Russia-Ukraine War, which has not yet come to an end, posing major challenges related to geopolitical risks. The trend of the Central Bank raising interest rates to cope with inflation has not ended as inflation is still increasing on a large scale. The trend of public debt increasing especially in some European countries. Recession and slow growth occurred in many major economies.

With influences from the world economy, the domestic economy cannot avoid risks such as inflation, which is likely to peak later than other countries in the world, pressure from interest rates, and factors related to economic growth. geopolitical risks. However, with the expectation of continued recovery after the pandemic in the food service, tourism service, and manufacturing technology industries along with being part of a series of free trade agreements, Vietnam still has can have long-term growth potential, despite short-term negative macroeconomic factors. Growth forecast for 2023 could reach 5.8%-6.2%.

In the context of world inflation putting pressure on major economies in the world, the inflation target in 2022 is still maintained at an increase of less than 4%, specifically inflation has increased by 3.15% compared to 2021, reaching goals set by the National Assembly. In the base scenario, inflation in 2023 is forecast to be about 4.5% – 5%. In which, the period of peak inflation forecast with high monthly increases may fall during the Lunar New Year period in the first quarter of 2023.

Context 2022: Consumer price index (CPI) in December 2022 decreased by 0.01% compared to the previous month, increased by 4.55% compared to December 2021. For the whole year 2022, the average CPI increased by 3.15% compared to 2021, reaching the target set by the National Assembly.

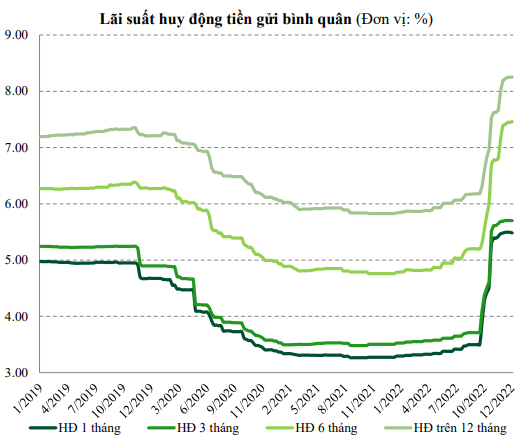

In order to restrain the rise of inflation, interest rates around the world have increased by 3-4% in the past year. Domestic interest rates from the beginning of the year to now have also increased by about 2.3% – 2.7%. VCBS believes that the increasing trend of deposit interest rates is also considered a reasonable response when interest rates in many countries are in an increasing trend. In 2023, it is likely that the process of raising interest rates by major central banks in the world will continue at least until June 2023. Deposit interest rates are forecast to increase by at least 100-150 basis points (1%-1, 5%) and although lending interest rates have a lag and the increase may be lower than deposit interest rates, it is expected that there will still be room to increase.

Outstanding credit debt in 2022 is estimated to increase by about 14.5% compared to the beginning of the year. Meanwhile, deposit mobilization through organizations and residents achieved a growth rate of 5.99% as of December 21. Deposit interest rates since the beginning of the year have increased by about 230-270 basis points.

Bond market

Pressure from the trend of increasing interest rates causes capital costs to be higher, closing in 2022. Interbank interest rates maintain a high level and are forecast to fluctuate around 7%, higher than the average year. In particular, short terms may fluctuate at lower levels in conditions where investment capital flows have more favorable developments than expected. It is forecast that 10-year bond interest rates are likely to peak around 5.5% with the peak period in the first 6 months of the year.

The first 6 months of the year witnessed a sharp increase in short-term bonds, making the yield curve tend to be flatter. Meanwhile, the last 6 months of the year is the period when the yield curve shifts strongly upward.

Market share

VN Index peaked at 1530 in April and began to enter a downtrend. Faced with negative information about inflation and the risk of global economic recession, the Vietnamese stock market moved in sync with the world stock market and continuously sought new bottoms, reaching the lowest level of 911.9 points. at mid-November 2022. In the last weeks of 2022, although liquidity decreased, bottom-fishing demand returned, helping revive the market and causing the VN Index to recover to over 1,000 points by the end of the year.

VN Index peaked at 1,530 in April and began to enter a downtrend. Faced with negative information about inflation and the risk of global economic recession, the Vietnamese stock market moved in sync with the world stock market and continuously sought new bottoms, reaching the lowest level of 911.9 points. at mid-November 2022.

It is forecasted that the Vietnamese stock market in 2023 will likely tend to fluctuate sideways within a large range of scores, with average liquidity likely to be significantly lower than in 2022. Many indexes It is likely that the score will fluctuate in the range of about 900 – 1,200 points, with the highest level of the index possibly reaching 1,250 points – equivalent to a decrease of nearly 18% compared to the peak of 2022. However, the index also has There may be a time when it will fall to about 900 points in the context that the FED continues to increase interest rates in the first half of 2023.

In 2022, many large-cap stocks will face strong selling pressure and negatively affect the trend of the general index such as VIC, NVL, VHM, HPG, GVR. There are only a few stocks that still maintain stable market prices such as BCM, SAB, GAS, BID and PNJ, helping the index somewhat limit the downward inertia.

Since the beginning of 2022, foreign investors still bought the most net shares of STB, DGC, CTG, DPM and FUEVFVND fund certificates. On the contrary, large-cap stocks such as HPG, VIC, NVL, MSN and EIB were the stocks with the strongest net selling since the beginning of the year.

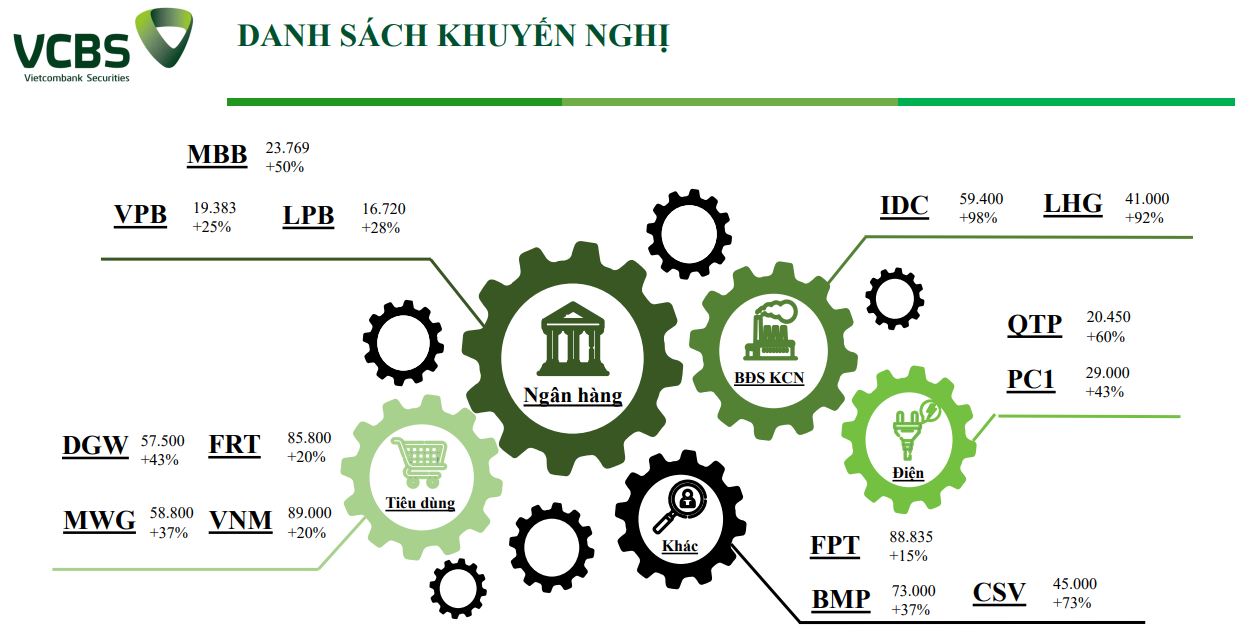

Some investment suggestions for 2023

1- Banking industry

Banking industry stocks are the group that accounts for the largest proportion of liquidity and capitalization in the Vietnamese stock market. In general, the business results of banks will be affected to a certain extent by the not so positive macroeconomic outlook in 2023. However, the banking group with good credit quality is likely to continue to receive positive credit limit allocation in 2023 and accordingly continue to maintain a positive growth trajectory. Stocks worth noting:

+ MBB: Projected 23,769 (+50%)

+ LPB: Forecast 16,720 (+28%)

+ VPB: Forecast 19,383 (+25%)

2- Real estate

The fact that state management agencies strictly handle businesses with violations in the real estate sector along with the ability to access loans is more difficult in the context of rising interest rates, causing short-term prospects. The term of both residential real estate and industrial real estate is less positive. But in the long term, the growth potential of the industrial park real estate sector is still huge along with the process of expanding infrastructure in Vietnam to serve the goal of industrialization and modernization. . Summarizing the factors, we think that during this period, investors can screen out industrial park real estate businesses that are in the sales cycle (not in the project implementation stage). have a low debt-to-equity ratio and choose the disbursement time when the market recovers after successfully establishing a medium-term bottom. Stocks worth noting:

+ IDC: Forecast 59,400 (+98%)

+ LHG: 41,000 (+92%)

3- Other industry groups

Stocks in “defensive” industries with business results less dependent on the economic cycle than other industries will likely also be less negatively affected in the outlook of major economies. and are also Vietnam’s major trading partners facing the risk of economic recession in 2023. On the other hand, these are all industry groups that have had a certain recovery since mid-2022 after Vietnam concluded end the period of social distancing. In the current context of the Vietnamese stock market, we believe that such stocks will lean more towards transportation, information technology & telecommunications and utility industries such as hydropower, thermal power, water supply,…

+ DGW: 57,500 (+43%)

+ FRT: Projected 85,800 (+20%)

+ MWG: Forecast 58,800 (+37%)

+ VNM: Forecast 89,000 (+20%)

+ QTP: Projected 20,450 (+60%)

+ PC1: Projected 29,000 (+43%)

In addition, investors can also look for opportunities in stocks with stable net cash flow from operating activities and a cash dividend payout ratio compared to the stock market price (D/P). ) is higher than the savings interest rate. These will usually be state-owned enterprises and use a large proportion of annual after-tax profits to pay cash dividends.

+ FPT: Projected 88,835 (+15%)

+ BMP: Projected 73,000 (+37%)

+ CSV: Projected 45,000 (+73%)

👉See report details in the Analytical Report section on TOPI application: https://app.topi.vn/fbpost

Disclaimer: This report and/or any comments and information in this report are not offers to buy or sell any financial products or securities analyzed in the report and are not Any investment consulting products or investment consulting opinions of VCBS or units/members related to VCBS. Therefore, investors should only consider this report as a reference source. VCBS does not accept any responsibility for unintended results when you use the above information to trade securities.

Source: VCBS 2023 outlook report